Tax Savings & Corporate Wealth Transfer Conference for Doctors Only

Exclusive Event – Fine Dining Experience

April 11, 2026 (Saturday) · Vancouver

April 12, 2026 (Sunday) · Vancouver

April 18, 2026 (Saturday) · Toronto

April 19, 2026 (Sunday) · Toronto

April 26, 2026 (Sunday) · Calgary

Hear From Past Attendees

Watch highlights and real conversations from past conferences — featuring Canadian doctors just like you.

Tailored for Experienced Doctors

This exclusive event is designed for incorporated doctors who want to reduce taxes, protect assets, and strategically grow their wealth.

Hosted by GT Wealth, a team of planners with over 100 years of combined experience, we proudly serve top 1% income earners across British Columbia, Alberta, and Ontario. As a leading one-stop firm in tax savings and corporate wealth transferring, we specialize in strategies that deliver measurable, lasting results.

Tax Savings & Corporate Wealth Transfer Conference for Doctors Only

Exclusive Event – Fine Dining Experience

April 11, 2026 (Saturday) · Vancouver

April 12, 2026 (Sunday) · Vancouver

April 18, 2026 (Saturday) · Toronto

April 19, 2026 (Sunday) · Toronto

April 26, 2026 (Sunday) · Calgary

Choose the Topics That Matter Most to You

To ensure every guest receives maximum value, each session is limited to just 20 doctors. Attendees can select the topics that matter most to them, and our expert speaker will provide actionable insights on the relevant sections of the Income Tax Act to help you achieve targeted wealth creation and tax savings — ranging from millions to tens of millions.

✅Income Tax Act s. 15(1)

Use corporate assets to reduce tax when repaying a personal mortgage or acquiring personal property.

✅ITA s. 20(1)(c)

Transfer corporate assets to personal hands with a 50% tax offset and reduce passive income taxed at 50% to retain capital.

✅ITA s. 148

Withdraw RRSP/RRIF tax-efficiently; implement a self-insured retirement plan to minimize 50% tax and a 15% government claw back.

✅ITA s. 138.1

Invest through Canada, U.S., Europe, and Asia sector funds with 2–3× returns (2014–2024) and optional principal guarantees.

✅Income Tax Act s. 85

Transfer shares to family without immediate tax; mitigate deemed disposition capital gains tax of 25% at the estate.

✅ITA s. 104

Use trust structures to safeguard assets against mismanagement and protect from relationship breakdown.

✅ITA s. 73(1.01)

Transfer assets to an alter ego trust to avoid 5% probate fees and reduce the risk of family disputes.

Limited-Time Offer

Be among the first 20 confirmed doctors to register and attend free of charge. Your experience includes:

Fine Dining – Enjoy a three-course meal of your choice

Exclusive – Limited to doctors, and their partners

Private Q&A – 30-minute one-on-one interview

$500 Value Advice Memo – Initial report tailored to your chosen areas

Presented By - One of the most well-known high-net-worth speakers

Tax Savings & Corporate Wealth Transfer Conference for Doctors Only

Exclusive Event – Fine Dining Experience

April 11, 2026 (Saturday) · Vancouver

April 12, 2026 (Sunday) · Vancouver

April 18, 2026 (Saturday) · Toronto

April 19, 2026 (Sunday) · Toronto

April 26, 2026 (Sunday) · Calgary

Case Study No. 1: Dr. Client

Below is a preview of the tailor-made 10-page Advice Memo for Dr. Client, outlining key issues, proposed solutions, legal structures, and second-stage opportunities. If you’d like a customized Advice Memo, book a complimentary 30-minute Zoom consultation with our relationship advisor for tailored insights.

Dr. Client spent decades building wealth. However, when the financial structure is not properly designed, multiples of $1,000,000 may quietly disappear through taxation. Dr. Client’s situation is a common case among high earning corporate owners who consult us to diagnose their financial structure.

1. Mortgage structure problem. Interest on a principal residence mortgage is not tax deductible under Income Tax Act s.18(1)(b) and the interest deductibility principles under s.20(1)(c).

If Dr. Client wants $1,000,000 personally to repay the mortgage, the corporation must distribute about $1,900,000 due to the approximately 48 percent tax on non eligible dividends. About $960,000 may be lost to tax before reducing the mortgage. Even after this cost, the mortgage interest remains non deductible because the borrowing relates to a principal residence rather than an investment.

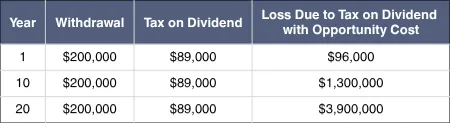

2. Gradual withdrawal problem. Some advisors recommend withdrawing smaller amounts over time.

Dr. Client’s corporation earns about $1,000,000 annually and distributes about $200,000 in dividends plus a $150,000 salary. If $200,000 is withdrawn annually, this equals $4,000,000 over 20 years.

However, the larger loss is compounding. At 7 percent annual growth, the lost reinvestment may reach about $1.3 million by year 10 and about $3.9 million by year 20.

3. Some advisors recommend retaining funds inside the corporation. If Dr. Client retains about $500,000 annually, the corporation may accumulate roughly $10,000,000 over 20 years.

If this capital earns about 5 percent interest, passive income inside a corporation may face tax approaching 50 percent under the passive income regime governed by ITA s.123.3 and an additional dividend tax of about 48 percent may apply under s.82 and s.121. The impact may look like this:

In year 1, the shareholder may receive about $270,000 after tax, while paying approximately $12,000 in passive income tax and $240,000 in dividend tax. By year 10, the after tax value may reach about $3.2 million, with roughly $140,000 paid in passive income tax and $3.2 million in dividend tax. By year 20, the shareholder may receive about $7.7 million after tax, while total taxes paid may reach approximately $8.4 million. As capital grows, tax leakage grows with it.

4. Retirement withdrawal assumption. Some advisors suggest waiting until retirement.

Assume Dr. Client needs $200,000 after tax annually. With a personal tax rate around 40 percent, the corporation may need to distribute about $330,000 annually, creating about $130,000 of tax each year under the dividend taxation rules in ITA s.82 and s.121. Over 30 years of retirement, annual tax may be about $130,000, resulting in total tax of approximately $3.9 million.

5. If funds remain in the corporation or RRSP or RRIF at death, deemed disposition rules apply under ITA s.70(5). Corporate assets may face multiple tax layers, and RRSP or RRIF may be treated as 100 percent taxable income. Even when withdrawals are delayed, tax leakage does not disappear. It spreads across decades, creating about $1,600,000 tax during retirement and another $1,500,000 at the estate level, totaling about $3,200,000.

Solutions

RRSP with Corporate Income Hedging and Interest Meltdown

Under Subsection 89(1) of the Income Tax Act (ITA), allow funds to grow within the company tax-efficiently and transfer them out through a Capital Dividend Account.

Under Paragraph 20(1)(c) of Income Tax Act, applying for an investment loan to create deductible interest expenses against annual income, as an alternative to making new RRSP contributions.

The above strategies can lower the tax by $2 million.

Under Section 148 of the Income Tax Act, the tax-exempt account allows for tax-deferred growth. By re-allocating $500k for 10 years into a tax-exempt account, the client could accumulate $20M by retirement.

Assign the policy to a third-party lender to secure a personal loan based on the cash value. Loan proceeds are received without triggering immediate tax, saving on $6 million taxes incurred on yearly cash flow.

Legal Document Coordination: Corporate Restructuring , Wills, Corporate Will.

✅ Corporate restructure with proper Opco and Holdco inter-company setup for $1 million tax defer transactions.

✅ Will: provides a foundational step in estate planning and ensures a seamless estate transfer, avoiding unnecessary delays and costs.

✅ Corporate Will: While Alberta has minimal probate cost, it's highly advisable to include a corporate succession plan in your Will for smooth business transition and continuity.

Additional Key Strategies to Be Reviewed After Above Priorities Are Addressed...

✅ Intergeneration Tax Saving Plan (ITSP)

✅ Alter Ego/Joint Partner Trust

✅ Estate Freeze

Tax Savings & Corporate Wealth Transfer Conference for Doctors Only

Exclusive Event – Fine Dining Experience

April 11, 2026 (Saturday) · Vancouver

April 12, 2026 (Sunday) · Vancouver

April 18, 2026 (Saturday) · Toronto

April 19, 2026 (Sunday) · Toronto

April 26, 2026 (Sunday) · Calgary

🎥 Real Questions From Canadian Doctors

📸 Gallery: Our Recent Event

CLIENT TESTIMONIAL

When discerning high-net-worth clients first approached corporate tax savings and estate planning services, they often grappled with hesitation. Ultimately, why did they choose GT Wealth?

The answer lies not only in GT Wealth's innovative approach of integrating top-tier accounting, legal, and financial professionals to deliver distinctive advice but also in its dedication to clients’ goals. At GT Wealth, the standard is nothing below the best, and the priority is ensuring that high-net-worth client receives 100% at the outset and 200% throughout the decades—a commitment reflected in their glowing testimonials.

Thank you to Dr. Lawrence L. for taking the time to provide such warm and thoughtful feedback to GT Wealth, despite his busy schedule managing multiple clinics in Vancouver and Calgary.

1. What unique value have our services brought to your financial journey?

With Mr. Lau and Ace’s help, we are now set up with a tax-efficient legacy planning for our family. More importantly, they have implemented an innovative strategy that allowed us to legally support our personal mortgage payments using the corporate profits in a tax efficient way. We wish we have known of your team earlier.

2. In what ways do you feel we stand apart from other advisory teams you’ve worked with?

Prior to meeting your team, we have discussed our situation and concerns with another similar team but your team has shown us much more thorough understanding about our particular case and could offer more efficient and sensible solutions. Your role as a quarterback coordinating with our accountants and providing us creative planning ideas, have impressed us tremendously. Your company’s business model is one of a kind among your industry’s peers.

3. What inspires your confidence to recommend us to other doctors or high-net-worth families?

I believe many of our friends who have accumulated decent wealth throughout their career years with their hard work and perseverance deserve a top notch professional team to help their estate planning. We are very happy to recommend your team to our circle of friends as I believe you will also do a fantastic job for them.

Tax Savings & Corporate Wealth Transfer Conference for Doctors Only

Exclusive Event – Fine Dining Experience

April 11, 2026 (Saturday) · Vancouver

April 12, 2026 (Sunday) · Vancouver

April 18, 2026 (Saturday) · Toronto

April 19, 2026 (Sunday) · Toronto

April 26, 2026 (Sunday) · Calgary

Case Study No. 2: Dr. Moha XXX

Below is a preview of the tailor-made 10-page Advice Memo for Moha, outlining key issues, proposed solutions, legal structures, and second-stage opportunities. If you’d like a customized Advice Memo, book a complimentary 30-minute Zoom consultation with our relationship advisor for tailored insights.

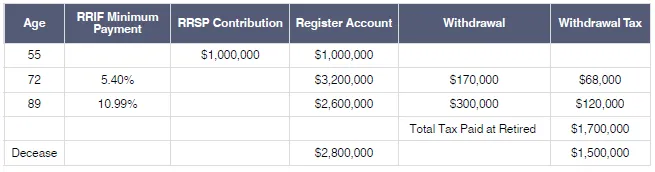

This accomplished doctor has built a $21.6 million portfolio across corporate holdings, real estate, and RRSPs. Their priorities are clear: unwind $2.8 million in RRSPs tax-efficiently and transition more than $12.6 million of corporate assets and investment real estate to their children with minimal tax erosion.

Despite their career success, their existing plan was sufficient for an average investor but inadequate to preserve long-term value. Through advanced structuring, Dr. Moha engaged us to reduce RRSP withdrawal taxes, facilitate efficient corporate and real estate transfers, and unlock an estimated $10 million in lifetime tax savings.

Key Financial Issues

➡️ Significant Final Tax Liabilities

Under Section 70(5) of the Income Tax Act, all capital assets are deemed disposed of at death, triggering substantial tax. Projected Estate Value (5% growth assumption): $76 million. Estimated Tax at Death: $19 million

➡️ Capital Gains on Dental Practice Sale

The dental practice is appraised at $3.5 million, with a significant capital gains tax upon sale. Estimated Capital Gains Tax: $875,000.

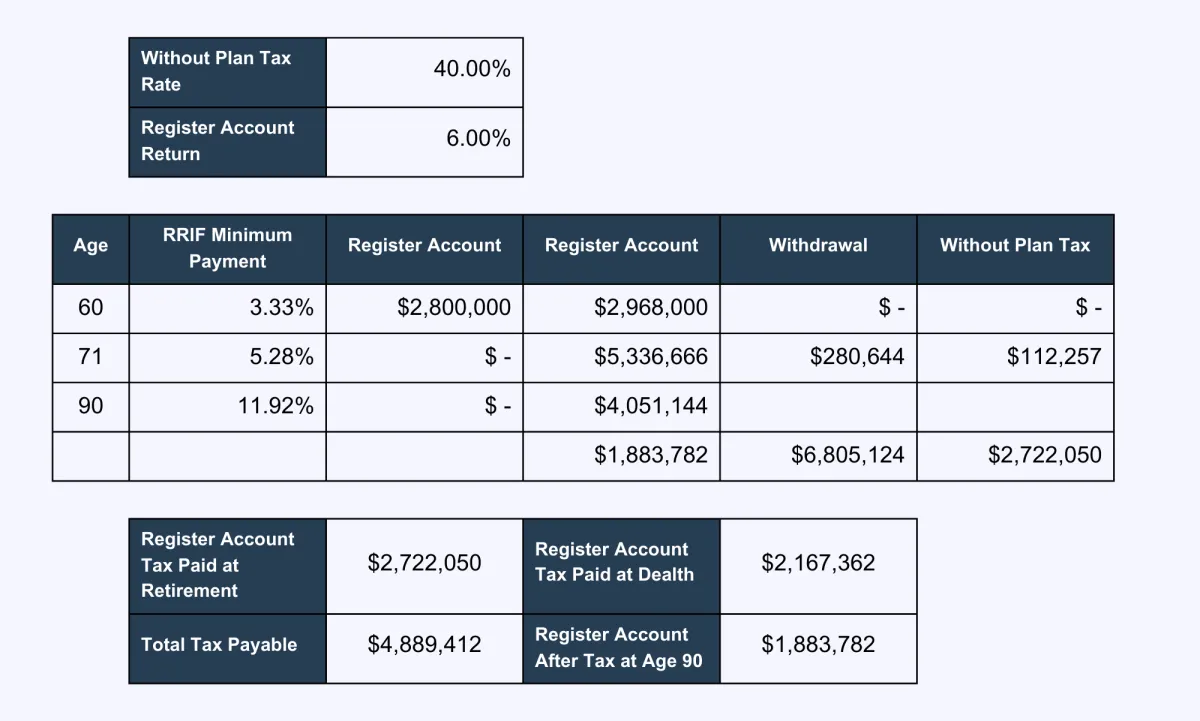

➡️ $2.8 million RRSP Tax Exposure

At age 71, RRSPs must convert to a RRIF, forcing taxable withdrawals on a minimum schedule. Projected Taxes During Lifetime Withdrawals: $2.72 million. Remaining RRSP at Age 90: $4.05 million — fully taxable at death, creating an additional $2.16 million tax liability. Total of $4.88 million taxes paid for the lifetime of RRSP redemption.

Solutions

✅ Estate Freeze

(Income Tax Act Section 86 & 51)

Lock in today’s asset values for tax purposes and pass future growth to the next generation tax-efficiently. You keep preferred shares equal to the current asset values, while your child receives common shares starting at zero value. All future growth accrues to the common shares.

➡️Example: $12.6M real estate portfolio projected to $42.6M in 25 years.

➡️Without planning: ~$8.9M tax.

➡️With Estate Freeze: ~$1.4M immediate exposure — a $7.5M reduction.

✅Lifetime Capital Gains Exemption (LCGE)

(Income Tax Act Section 110.6)

Shelter up to $1.25M of capital gains from tax when selling shares of a Qualified Small Business Corporation (QSBC).

➡️Qualification Criteria: Shares held >24 months by you or a related person; 50%+ of corporate assets in active Canadian business during that period; and 90%+ of assets in active Canadian business use at the time of sale.

➡️Impact: ~$312K in tax savings, with potential for an additional $500K through advanced structuring.

✅RRSP Meltdown Strategy

(Income Tax Act Paragraph 20(1)(c))

Leverage the interest meltdown strategy to gradually draw down RRSPs while reducing overall lifetime tax. By withdrawing $100,000 annually from your RRSP and using the proceeds for interest funding, these interest payments become fully deductible against your personal income.

➡️Results: $2M transferred from RRSP with ~$1.07M tax savings, while also reducing tax payable at both withdrawal and death.

Additional Key Strategies to Be Reviewed After Above Priorities Are Addressed...

✅Family Trust

Asset protection & income splitting

✅Shared-Ownership Plan

Income protection and a guaranteed retirement fund via tax free corporate funding reimbursement via this plan

✅Health Spending Account (HSA)

Tax efficient way for personal medical expenses through your corporation

✅Property Tax Savings Program

Utilize on annual property taxes immediately

Tax Savings & Corporate Wealth Transfer Conference for Doctors Only

Exclusive Event – Fine Dining Experience

April 11, 2026 (Saturday) · Vancouver

April 12, 2026 (Sunday) · Vancouver

April 18, 2026 (Saturday) · Toronto

April 19, 2026 (Sunday) · Toronto

April 26, 2026 (Sunday) · Calgary

Updated in 2025

20+

New Conferences

1,000+

New Doctors & Dentists Consulted

$100 millions+

New Wealth Managed

Tax Savings & Corporate Wealth Transfer Conference for Doctors Only

Exclusive Event – Fine Dining Experience

April 11, 2026 (Saturday) · Vancouver

April 12, 2026 (Sunday) · Vancouver

April 18, 2026 (Saturday) · Toronto

April 19, 2026 (Sunday) · Toronto

April 26, 2026 (Sunday) · Calgary

Book a complimentary 30-minute Zoom consultation with our relationship advisor for tailored insights.

FOLLOW US

For ticket inquiry, please contact our high net worth team: 604-910-0124

Our Offices:

405 - 6388 No. 3 Road, Richmond, BC

Metro Tower II, Suite 2660-4720 Kingsway, Burnaby, BC

N500 - 675 Cochrane Drive North Tower, Markham, ON

9140 Leslie Street, Suite 208, Richmond Hill, ON